Auto Insurance- FAQ

Blog Post by Madison D’Angelo

November 18th, 2014

Looking for Auto Insurance?

When it finally comes time to purchase auto insurance, many of us are left in the dark when it comes to knowing what exactly we are paying for and how we will be covered if the need arises. Below is a bit of basic information that answers some of the most frequently asked questions when it comes to auto insurance:

Terms and Definitions:

Provided by the Insurance Bureau of Canada

Automobile Insurance- Insurance coverage that provides indemnity and/or compensation for injury or physical damage which ensues from the ownership, use or operation of an automobile.

CLEAR- CLEAR is the Canadian Loss Experience Automobile Rating. This is a method for classifying different models of cars for insurance purposes by using historical claims data, including Collision, Comprehensive, Direct Compensation – Property Damage, and Accident Benefits coverages. CLEAR is used by many insurance companies across the country.

Collision Coverage- An optional type of automobile insurance coverage that pays for the cost of repairing the insured vehicle if it is damaged in a collision or upset. In some parts of the country, this is referred to as “Section C.”

Compulsory Insurance- Any form of insurance (usually auto insurance) that is required by law.

Deductible- An agreed specified sum to be deducted from the amount of loss and assumed by the insured.

High-Risk Automobile Insurance Market- Consumers with a poor driving record (e.g., multiple driving infractions, demerit points or criminal convictions involving driving), or no driving record at all (i.e., new drivers), may, in many cases, be insured by insurance companies that specialize in drivers who are high risk.

Liability- This is a legally enforceable obligation. Liability insurance pays for the damages or losses suffered by others for which the insured person is legally responsible.

Optional coverage- In automobile insurance, optional coverage is a commonly used term for insurance that is not required by law, such as coverage for collision or comprehensive claims (e.g., theft).

Premium- An insurance premium is the money the policyholder pays to the insurer for financial protection against specific risks for a specific time-span. Unlike the premiums for many forms of life insurance, general insurance premiums are not intended to produce a reward other than financial peace of mind.

Red Book– Canadian publication which lists the values of automobiles, including their wholesale and average retail price, used as a guide by automobile dealers, claims adjusters etc., to establish market value of used automobiles. American version of this publication is called a “Blue Book”.

Total Loss- Loss of all the insured property. Also a loss involving the maximum amount for which a policy is liable.

Frequently Asked Questions:

- What coverage is mandatory and what is optional?

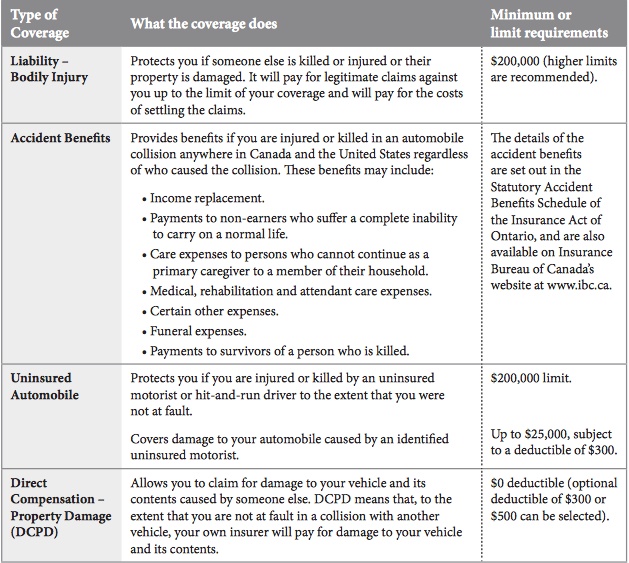

Auto insurance is mandatory in Ontario, however, not all types of coverage are compulsory. The tables below indicate the mandatory vs. optional coverages and how they work.

Mandatory Coverage:

NB: Although collision and comprehensive coverage are not compulsory, if you owe money on your vehicle, your lien-holder may require you to have these types of coverage to protect their interest in your vehicle.

- What affects my premium?

Your premium is affected by many different factors. To establish a premium, here are a few of the things that the insurance companies will take into consideration:

- The year, make and model of your vehicle

- The distance you drive annually

- The age and driving experience of all the listed drivers

- The claims and collision history of the drivers

- What is No-Fault insurance?

No-fault Insurance doesn’t mean that if you cause a collision, the insurance company lets you off the hook. No-fault simply means that regardless of who caused the collision, you can deal with your own insurance company for settling injury and collision damage.

- What happens when my vehicle is a total loss?

A “Total Loss” occurs when the repairs to the vehicle damage are not economically or safely able to be carried out. For example, if the cost of repair would be greater than the actual worth of the vehicle. Your insurance company will calculate the cash value of the vehicle, including tax, and offer you a cash settlement, with which you can purchase a new car. Make sure your insurance company is informed of any work you may have done that would increase the selling price of your vehicle (you may need to provide receipts).

If you are curious about an insurance quote, contact us and we will send you some approximate quotes based on the vehicles we offer.